NY GHG Disclosure · S9072A

Preparing for the Climate Corporate Data Accountability Act

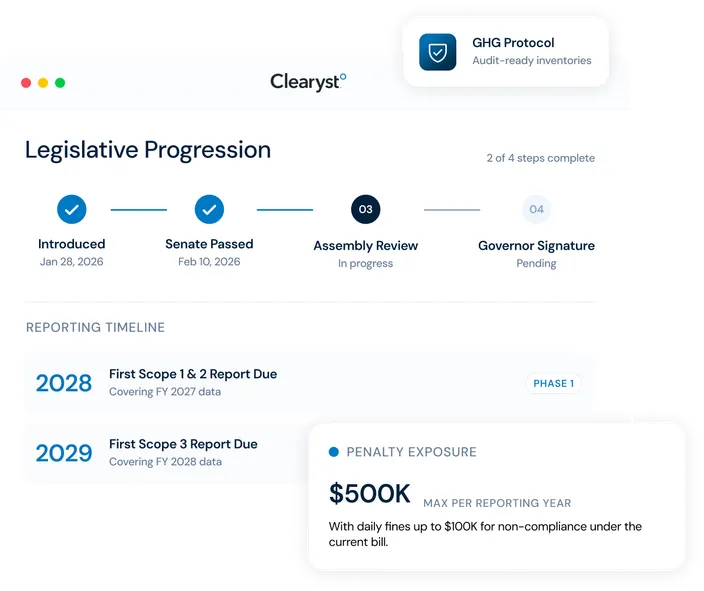

New York's Climate Corporate Data Accountability Act would require U.S.-based companies with revenues over $1 billion to annually report Scope 1, 2, and 3 GHG emissions. Reporting would begin in 2028 for 2027 data, with Scope 3 following in 2029.

What Is the Climate Corporate Data Accountability Act?

A New York State bill (S9072A) that, if signed into law, would require U.S.-based companies with over $1 billion in annual revenue to publicly report their Scope 1, 2, and 3 greenhouse gas emissions each year. It closely mirrors California's SB 253, so for companies already tracking SB 253, this isn't a new direction, it's an expansion.

If Enacted, the Act Would

- Require annual reporting of Scope 1, 2, and 3 emissions

- Be overseen by the NY Department of Environmental Conservation

- Apply to U.S.-based companies exceeding $1 billion in revenue

- Align closely with California's SB 253 framework

Scope Definitions

- Scope 1: direct emissions from sources your company owns or controls, fleets, combustion, on-site fuel use

- Scope 2: indirect emissions from purchased energy, electricity, steam, heating, and cooling across operations

- Scope 3: value-chain emissions across upstream and downstream activities, suppliers, logistics, product use

How Does New York's Law Compare to California's SB 253?

| California SB 253 | NY CCDAA (S9072A) | |

|---|---|---|

| Revenue Threshold | $1B+ | $1B+ |

| Emissions Scope | Scope 1, 2, 3 | Scope 1, 2, 3 |

| Scope 1 & 2 Start | 2026 | 2028 |

| Scope 3 Start | 2027 | 2029 |

| Status | Active Law | Pending Assembly & Signature |

| Regulatory Body | CARB | NY DEC |

Build Once. Use Everywhere.

The inventory you build for California's SB 253 works for New York's CCDAA. Standardized, audit-ready emissions data lets you satisfy multiple state disclosure programs from a single source of truth, without duplicating the work each time a new law takes effect.

How Clearyst° Helps Companies Prepare for NY GHG Disclosure

A five-step path from applicability assessment to assurance-ready disclosure, built to serve New York, California, and your broader ESG reporting at once.

Scope and Applicability Assessment

Determines whether and when your company must comply with the CCDAA based on the $1 billion revenue threshold, organizational structure, and reporting entity definition. Outcome: clear direction so you invest in the right level of preparation.

- Confirm applicability based on revenue and structure

- Define reporting boundaries across entities

- Align NY requirements with SB 253 programs

GHG Inventory Development: Scope 1, 2, and 3

A systematic accounting of total greenhouse gas emissions across Scope 1, 2, and 3, the foundational requirement for compliance. Outcome: one inventory that supports NY, SB 253, and broader ESG reporting.

- Complete, audit-ready inventories aligned to GHG Protocol

- Standardized methodologies across business units

- Repeatable, scalable data structures

Data Collection and Management

Coordination across internal teams and external partners, especially for Scope 3 categories. Outcome: reliable data that reduces risk and improves efficiency each cycle.

- Cross-functional data collection processes

- Supplier engagement for Scope 3 data

- Year-over-year reporting systems

Reporting and Disclosure Preparation

Transforms your inventory into a structured, compliant report aligned with regulatory expectations. Outcome: a report that meets requirements and supports stakeholder transparency.

- Prepare disclosure-ready emissions reports

- Validate completeness and consistency

- Coordinate across multiple reporting frameworks

Assurance Preparation

Third-party verification of your emissions data. Outcome: reduced audit risk and stronger credibility from day one.

- Complete documentation and audit trails

- Clear methodologies and assumptions

- Readiness for future verification requirements

Why Start Building Your GHG Inventory Before the Law Takes Effect?

Scope 3 Takes Time

Data collection across suppliers and value chains cannot be built quickly or retroactively.

2027 Data Year Is Close

By the time the law is final, most teams will be behind on collection infrastructure.

SB 253 Overlaps

Aligning California and New York programs now eliminates duplicate work later.

Investors Already Ask

Customers and capital markets are requesting emissions data independent of regulation.

Frequently Asked Questions

What is the Climate Corporate Data Accountability Act?

A New York bill requiring companies with over $1 billion in revenue to report Scope 1, 2, and 3 emissions annually. It has passed the senate and is in the assembly, after which it will require the Governor's signature.

Which companies are in scope?

U.S.-based companies exceeding $1 billion in annual revenue, regardless of headquarters location.

When does reporting start?

Scope 1 and 2 reporting begins in 2028 (for 2027 data), with Scope 3 following in 2029.

What are Scope 1, 2, and 3 emissions?

Scope 1 is direct emissions, Scope 2 is purchased energy, and Scope 3 is value chain emissions.

How is this different from SB 253?

The requirements are similar, but SB 253 is already active. New York's law follows a similar structure with a later start date.

What does compliance involve?

Building a full GHG inventory, collecting and validating data, and preparing disclosures for verification.

'%20style='fill:%231672E7;fill:color(display-p3%200.0863%200.4471%200.9059);fill-opacity:1;'/%3e%3c/svg%3e)

'%20style='fill:%231672E7;fill:color(display-p3%200.0863%200.4471%200.9059);fill-opacity:1;'/%3e%3c/g%3e%3c/svg%3e)

'%3e%3ccircle%20cx='499.808'%20cy='499.808'%20r='399.808'%20fill='%231672E7'%20style='fill:%231672E7;fill-opacity:1;'/%3e%3c/g%3e%3cdefs%3e%3cfilter%20id='filter0_f_0_54'%20x='0'%20y='0'%20width='999.615'%20height='999.615'%20filterUnits='userSpaceOnUse'%20color-interpolation-filters='sRGB'%3e%3cfeFlood%20flood-opacity='0'%20result='BackgroundImageFix'/%3e%3cfeBlend%20mode='normal'%20in='SourceGraphic'%20in2='BackgroundImageFix'%20result='shape'/%3e%3cfeGaussianBlur%20stdDeviation='50'%20result='effect1_foregroundBlur_0_54'/%3e%3c/filter%3e%3c/defs%3e%3c/svg%3e)

Get Ahead of New York's GHG Disclosure Requirements

The timeline is approaching, even if the law is still pending. The right time to start building your GHG inventory is before reporting becomes mandatory.

The 2027 data year will arrive faster than it looks. Explore Our Sustainability Services →